You are using an out of date browser. It may not display this or other websites correctly.

You should upgrade or use an alternative browser.

You should upgrade or use an alternative browser.

ACS-64 Heads Up

- Thread starter Acela150

- Start date

Help Support Amtrak Unlimited Discussion Forum:

This site may earn a commission from merchant affiliate

links, including eBay, Amazon, and others.

- Status

- Not open for further replies.

KmH

Engineer

Look Ma! No hands!

Acela150

Super Buff

I could never grasp the concept of DPU's. Nice video!

PerRock

Engineer

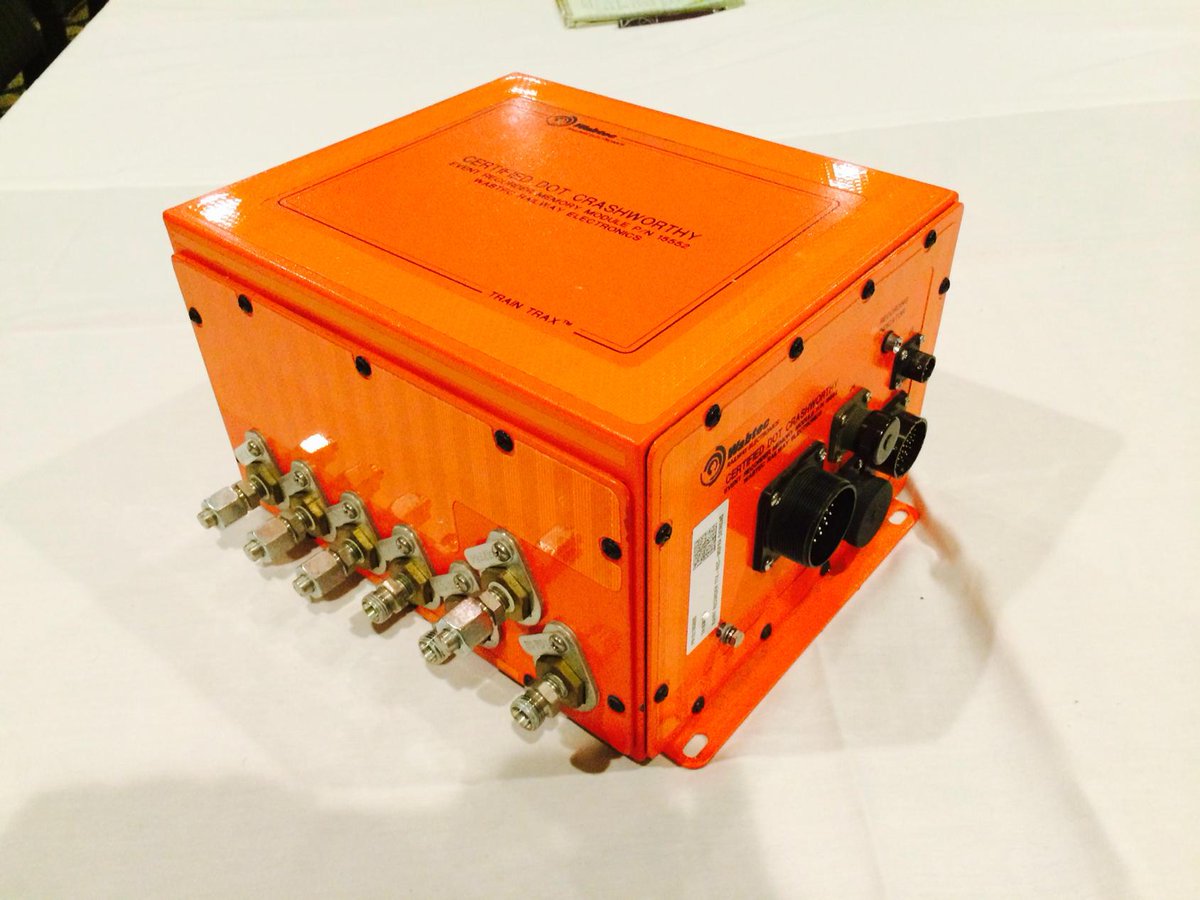

Not really a heads up, but the NTSB posted a picture of #601's data recorder, if anyone's interested, here is what the ACS-64 Black Boxes look like:

peter

peter

Ryan

Court Jester

Doesn't look very black to me.

(yes, I know they're all orange for visibility after a crash)

(yes, I know they're all orange for visibility after a crash)

Its official. Amtrak will not be the only operators of ACS-64s in the US. SEPTA has reached an agreement with Siemens to buy 13 ACS-64s with an option for 5 more. Philly.com: SEPTA plans to spend $154 million on new locomotives.

Excerpt:

Excerpt:

So in 2018, rail fans in SEPTA territory can start to look for Sprinters in SEPTA colors! The delivery timing makes sense as Siemens will be busy delivering Charger diesel locomotives to the states and AAF through 2018.SEPTA plans to spend up to $154 million for 18 new Regional Rail locomotives, the authority's biggest railroad acquisition in a decade.

The electric locomotives would replace eight aging engines operating on the Lansdale-Doylestown, Paoli-Thorndale, Trenton, and Wilmington-Newark lines, and to add capacity to other lines.

The SEPTA board is expected to approve the purchase on Thursday, with the locomotives to be delivered in 2018.

SEPTA is buying 13 "Cities Sprinter" ACS-64 locomotives to be built by Siemens Industry Inc., the German conglomerate, at its Sacramento, Calif., factory. The purchase price includes an option for five additional locomotives.

$16.99

$22.99

Fodor's Best Road Trips in the USA: 50 Epic Trips Across All 50 States (Full-color Travel Guide)

Amazon.com

MattW

Conductor

Excellent! Always great to see another operator making the right decision on locomotives (I'm looking at you MARC).

PerRock

Engineer

Does this mean that the "Amtrak Cities Sprinter" will become the "American Cities Sprinter"?

peter

peter

jis

Permanent Way Inspector

Staff member

Administator

Moderator

AU Supporting Member

Gathering Team Member

I guess they will also need to buy a few cars to attach those locomotives to. At present they have about 50 trailers and 8 locomotives.

Yes. As the news article states: "And it will soon begin the process of procuring 45 bi-level railcars to increase capacity on the Regional Rail lines." So the SEPTA ACS-64s will be teamed with new bi-level cars for rush hour trains.Hasn't SEPTA been looking a bilevel equipment? Perhaps to pair with the new locomotives?

jis

Permanent Way Inspector

Staff member

Administator

Moderator

AU Supporting Member

Gathering Team Member

Amtrak will do anything for a suitable cash incentive.A couple questions popped into my mind.

Would these be "SCS-64s" instead of ACS-64s?

How would these be transported from California? Would Amtrak be willing to give SEPTA units a ride?

Even if they won't I am sure UP or BNSF together with CSX or NS would be happy to oblige. Nice addition to a hot shot I should think. George K

Conductor

At about $2/mile, they'll haul PV - why not another locomotive?Amtrak will do anything for a suitable cash incentive.

Last edited by a moderator:

Ugh, that's what I get for posting before reading...Yes. As the news article states: "And it will soon begin the process of procuring 45 bi-level railcars to increase capacity on the Regional Rail lines." So the SEPTA ACS-64s will be teamed with new bi-level cars for rush hour trains.Hasn't SEPTA been looking a bilevel equipment? Perhaps to pair with the new locomotives?

neroden

Engineer

Yeah, seriously, MARC should get with the program... not to mention the MBTA.Excellent! Always great to see another operator making the right decision on locomotives (I'm looking at you MARC).

Last edited by a moderator:

Ryan

Court Jester

Too bad that isn't going to happen, as they're planning on going all diesel.

Between the cost of the electricity to run them and paying Amtrak to maintain them, it costs MARC almost twice as much per mile to operate an electric motor over their diesels, and they don't have that kind of money to throw around.

Between the cost of the electricity to run them and paying Amtrak to maintain them, it costs MARC almost twice as much per mile to operate an electric motor over their diesels, and they don't have that kind of money to throw around.

Speaking of SEPTA, is it the *right* decision, or just a better decision? Would going all-EMU (whether bilevel or single-level as now) make more sense? Honest question, as EMUs seem to be the more typical standard outside of North America. I suppose there may not be bilevel EMUs in service in North America that fit the clearances in the Northeast, but they do exist elsewhere - and if Caltrain can get a waiver from FRA standards to operate different equipment then SEPTA could certainly try as well.Yeah, seriously, MARC should get with the program... not to mention the MBTA.Excellent! Always great to see another operator making the right decision on locomotives (I'm looking at you MARC).

As for MARC and MBTA, it's absurd that our fragmented/disjointed/backwards rail "network" and "planning" leads to such situations. Amtrak's interests are served by having commuter trains operate as quickly (both top speed and acceleration) as possible and I have to imagine that optimizing the equipment operated is overall less expensive than expanding track capacity.

jis

Permanent Way Inspector

Staff member

Administator

Moderator

AU Supporting Member

Gathering Team Member

If things like that actually bothered Amtrak enough they could incentivize the use of electric equipment by suitably adjusting traction power rates charged. but as long as traction power rates charged makes the effective cost of operating a train using electric engines more expensive than doing the same with diesel engines, there is very little incentive for an operation for which the Amtrak route is the only electric route, to operate it using electric power. As they say, follow the money and you will see the reason. It is no surprise that on the NEC only those outfits that must operate electrically do so. Not any of the others.

jis

Permanent Way Inspector

Staff member

Administator

Moderator

AU Supporting Member

Gathering Team Member

Bringing the whole thing back to the ACS-64, here is one of the best annotated photo of the Engineer's controls of the ACS-64 that I have come across anywhere:

http://www.philly.com/philly/news/Inside_the_cab_of_Train_188.html

http://www.philly.com/philly/news/Inside_the_cab_of_Train_188.html

neroden

Engineer

I don't know what rates Amtrak charges for traction power; I've never heard an actual quote. I have a sneaking suspicion that they're not outlandish. There is one thing which would cause them to appear unreasonable to *MARC*, though -- the going rates for both electricity and diesel vary wildly by region.

Amtrak gets its electricity for the the NEC from a very specific -- and expensive -- list of sources:

(North end)

Branford, CT (Eversource Energy / CL&P, EIA suggests 15.42 cents average price for this utility)

New London, CT (Eversource Energy / CL&P)

Warwick, RI (National Grid / Narraganset Electric, EIA suggests 14.34 cents average price)

Sharon, MA (National Grid or Eversource, I'm not sure which)

(South end)

Safe Harbor Dam (probably the cheapest, no public pricing available)

Metuchen NJ Rotary Converter (Public Service Co., very expensive electricity, EIA suggests 14.82 cents)

Lamokin PA Rotary Converter (Probably PECO, very expensive electricity, EIA suggests 13.92 cents -- or is it PP&L?)

Sunnyside NY Static Converter (ConEd, easily the most expensive electricity, EIA suggests 23.85 cents)

Richmond PA Static Converter (PECO, or is it PP&L? -- PP&L is only 12.22 average)

Jericho Park MD Static Converter (Baltimore Gas & Electric / Exelon, 13.43 cents)

By contrast, in upstate NY closer to Niagara Falls, I pay 11 cents.

If Amtrak is charging the same price for traction power along its entire system, that price will reflect an average of the costs along the length of the system. The north end is a lot more expensive than the south end and NYC is most expensive of all. If this is averaged, it may have the effect of high pricing as it appears to MARC.

Incidentally, ConEd / New York City prices are *so* high and rising *so* fast that in a few years it will probably be cost-effective for Amtrak to retire the Sunnyside converter in favor of banks of batteries such as the "utility scale" ones Tesla is producing (which are dropping in price), and use them to store electricity bought from cheaper utilities down the line.

Meanwhile, diesel in the PADD 1B region at $3.143. This is the second highest priced region in the country -- only on the west coast is it more expensive -- but it's cheap by historical standards.

MARC is still totally wrong to commit to diesels, because the price of diesel is not going to drop, and is very likely to go up, certainly to $4/gallon. The price of electricity, however will start dropping as solar reaches grid parity and the big solar deployments start going in. At some point it'll be clearly more expensive to run diesels... and I doubt that the MARC board has done its Levelized Cost estimates over the 20+-year-lifetime of the locomotives.

(Well, that was a fun hour browsing EIA statistics.)

Amtrak gets its electricity for the the NEC from a very specific -- and expensive -- list of sources:

(North end)

Branford, CT (Eversource Energy / CL&P, EIA suggests 15.42 cents average price for this utility)

New London, CT (Eversource Energy / CL&P)

Warwick, RI (National Grid / Narraganset Electric, EIA suggests 14.34 cents average price)

Sharon, MA (National Grid or Eversource, I'm not sure which)

(South end)

Safe Harbor Dam (probably the cheapest, no public pricing available)

Metuchen NJ Rotary Converter (Public Service Co., very expensive electricity, EIA suggests 14.82 cents)

Lamokin PA Rotary Converter (Probably PECO, very expensive electricity, EIA suggests 13.92 cents -- or is it PP&L?)

Sunnyside NY Static Converter (ConEd, easily the most expensive electricity, EIA suggests 23.85 cents)

Richmond PA Static Converter (PECO, or is it PP&L? -- PP&L is only 12.22 average)

Jericho Park MD Static Converter (Baltimore Gas & Electric / Exelon, 13.43 cents)

By contrast, in upstate NY closer to Niagara Falls, I pay 11 cents.

If Amtrak is charging the same price for traction power along its entire system, that price will reflect an average of the costs along the length of the system. The north end is a lot more expensive than the south end and NYC is most expensive of all. If this is averaged, it may have the effect of high pricing as it appears to MARC.

Incidentally, ConEd / New York City prices are *so* high and rising *so* fast that in a few years it will probably be cost-effective for Amtrak to retire the Sunnyside converter in favor of banks of batteries such as the "utility scale" ones Tesla is producing (which are dropping in price), and use them to store electricity bought from cheaper utilities down the line.

Meanwhile, diesel in the PADD 1B region at $3.143. This is the second highest priced region in the country -- only on the west coast is it more expensive -- but it's cheap by historical standards.

MARC is still totally wrong to commit to diesels, because the price of diesel is not going to drop, and is very likely to go up, certainly to $4/gallon. The price of electricity, however will start dropping as solar reaches grid parity and the big solar deployments start going in. At some point it'll be clearly more expensive to run diesels... and I doubt that the MARC board has done its Levelized Cost estimates over the 20+-year-lifetime of the locomotives.

(Well, that was a fun hour browsing EIA statistics.)

neroden

Engineer

So MARC should maintain new electric motors itself -- or pay SEPTA to maintain them, since SEPTA will have its own fleet of ACS-64s. They're cheaper to maintain than diesels;. If Amtrak is overcharging for maintenance, do it somewhere else -- it's not like they don't have options.Too bad that isn't going to happen, as they're planning on going all diesel.

Between the cost of the electricity to run them and paying Amtrak to maintain them, it costs MARC almost twice as much per mile to operate an electric motor over their diesels, and they don't have that kind of money to throw around.

Amtrak has a monopoly on traction power supply and is presumably overcharging somewhat, but I honestly can't believe the claims that they would cost twice as much per mile to operate. Is MARC perhaps comparing new diesels with old, non-regenerative-braking AEM-7s? Or with the shop-queen high-power-draw HHP-8s? MARC should be comparing them with ACS-64s, obviously. I suspect MARC of having made an apples-to-oranges comparison.

King County Metro (Seattle) issued a hatchet job report on its trolleybuses a couple of years ago comparing brand new fuel buses with their 20-year-old Bredas rather than comparing them with brand new New Flyer trolleybuses -- local activists cried foul, got after them, and King County Metro ended up issuing a new report which showed that yes, trolleybuses were cheaper to operate.

I can't find energy efficiency numbers for the MP40s. So take an optimistic 2.1 gallons per mile, based on Amtrak's performance -- that's $6.60 per mile now, but $8.40 per mile when diesel goes back to $4/gallon, as it will, and as it was when MARC's decisions were being made.

I have had difficulty finding the average energy efficiency of the ACS-64s in kwh/mile. So I guesstimated. The ACS-64 weighs 215,537 lb., while the Bombardier bilevels weigh approximately 134,880 lb, and there are typically 7 of them. Extrapolate from the energy efficiency of my electric auto, accounting for the extra mass, and you should be able to get 82.9 kwh/mile. (This is quite pessimistic because steel-on-steel has better traction than rubber-on-asphalt, and railroads have much shallower grades than the roads I drive on.)

At this rate, in order for electric traction to beat $4 diesel (disregarding maintenance) it would have to cost 10.1 cents / kwh or less. This is based on optimistic assumptions for diesel and pessimistic assumptions for electricity. So diesel may look cheaper *now*, but not *half* as expensive. Amtrak's presumably charging more than that, due to the inflated utility company prices along the corridor, but is Amtrak seriously charging 20 cents / kwh? I suppose it's possible.

I still doubt that MARC has done a proper apples-to-apples analysis with a 20-year cost projection.

Thirdrail7

Engineer

- Joined

- Jul 9, 2014

- Messages

- 4,542

Neroden:

While I still believe that you are probably correct in the assumption that a true apples to oranges analysis probably hasn't occurred, I'm not convinced that keeping electrics is the proper course of action based upon a previous statement you made:

There will only be one source of parts and that is Siemens.Since MARC subcontract their operations, I don't foresee them jumping into the locomotive maintenance in the new future. If they do not plan to deal with Amtrak, they would have to depend on SEPTA, which is an agency that never even overhauled their electrics. Additionally, how much would it cost MARC to have SEPTA maintain their equipment? By the time you deadhead the unit to wherever they plan to repair their units, it can be gone for weeks.

There is something to be said for a common fleet that can go anywhere, at any time. You can't say that when you have electrics involved unless the entire territory is or will be electrified. MARC will no longer have to bench certain trains at certain times or pay a switching crew to handle the electrics.

While I still believe that you are probably correct in the assumption that a true apples to oranges analysis probably hasn't occurred, I'm not convinced that keeping electrics is the proper course of action based upon a previous statement you made:

MARC would likely only order 10 electrics to replace their current fleet. Combine that with Amtrak's 70 units and Septa's 15 (max) order and it pales in comparison to the size of the MPI fleet that spans the nation. It is a small, specialized class of equipment.One of the lessons of the HHP-8s -- not a new lesson -- is that small classes of equipment are a bad idea. With a large class of HHP-8s, I could imagine all the bugs being worked out, the biggest problems being retrofitted, and stockpiles of spare parts. With a small class, there certainly weren't stockpiles of spare parts, and it was hardly worth retrofitting such a small class in any way...

There will only be one source of parts and that is Siemens.Since MARC subcontract their operations, I don't foresee them jumping into the locomotive maintenance in the new future. If they do not plan to deal with Amtrak, they would have to depend on SEPTA, which is an agency that never even overhauled their electrics. Additionally, how much would it cost MARC to have SEPTA maintain their equipment? By the time you deadhead the unit to wherever they plan to repair their units, it can be gone for weeks.

There is something to be said for a common fleet that can go anywhere, at any time. You can't say that when you have electrics involved unless the entire territory is or will be electrified. MARC will no longer have to bench certain trains at certain times or pay a switching crew to handle the electrics.

jis

Permanent Way Inspector

Staff member

Administator

Moderator

AU Supporting Member

Gathering Team Member

Have you taken into consideration the cost of maintaining two separate locomotive fleets? It seems to me that if you are forced to maintain a significant diesel fleet and need an electric fleet for just one line, a fleet that you can do without, that is something that should be taken into consideration. I don't think electric rates is the only issue, but it could be an issue that broke the camels back, in a manner of speaking.MARC is still totally wrong to commit to diesels, because the price of diesel is not going to drop, and is very likely to go up, certainly to $4/gallon. The price of electricity, however will start dropping as solar reaches grid parity and the big solar deployments start going in. At some point it'll be clearly more expensive to run diesels... and I doubt that the MARC board has done its Levelized Cost estimates over the 20+-year-lifetime of the locomotives.

(Well, that was a fun hour browsing EIA statistics.)

NJTransit actually has claimed in the past that they pay a higher rate for power on the Amtrak supplied part of the network than they pay for commercially sourced power for their 25kV electrification. I have no idea how they even figure out what they pay Amtrak, since AFAIK they do a gross up amount handshake once every couple of years for trackage and power. I suppose they use some per unit number to do the grossing up and that is what they are talking about.

Amtrak at one point tried to get itself declared an utility since it delivers power to others, to get some rate advantage. but that attempt was denied by the powers that be. Maybe PRR remembers the details. Also PRR being a retiree from an electric utility company, may have insights into this which he may or may not be willing to share.

- Status

- Not open for further replies.

Latest posts

-

-

-

-

-

Acela 21 (Avelia Liberty) development, testing and deployment (2025)

Acela 21 (Avelia Liberty) development, testing and deployment (2025)- Latest: JuniusLivonius